Potemkin

Predaceous Stink Bug

- Messages

- 213

- Reaction score

- 1

- Points

- 0

Welcome to the PMBug forums - a community supported watering hole for folks interested in gold, silver, precious metals, sound money, investing, market and economic news, central bank monetary policies, politics and more.

Register a free account to join the discussions. When you register an account and log in, you may enjoy additional benefits including access to market data/charts and additional members only rooms (including one for trade/barter with the community).

So I think there is a case to say that negative GOFO as more driven by tightness in the gold leasing market. Note that shortage in the borrowing and lending market does not have to coincide with a shortage in the buying and selling market.

A real gold bank run will manifest itself in the wholesale markets for 400oz bars. When I see them attracting a premium and/or being difficult to source, or bullion banks desperately bidding on the Perth Mint's refining output, then we "have the real deal" as Dan says. I will let you know. just watch Bullion Vault and Gold Money - which are backed by 400oz bars and which deal in that market every day - for reports of difficultlies in getting 400oz bars and restrictions on how much gold can be bought, and/or if they start to add on a "special" premium to their spot price.

http://www.gold.org/ (Q2 Market update)The Perth mint reported the highest demand levels in five years and that the mint was working through weekends to satisfy demand.

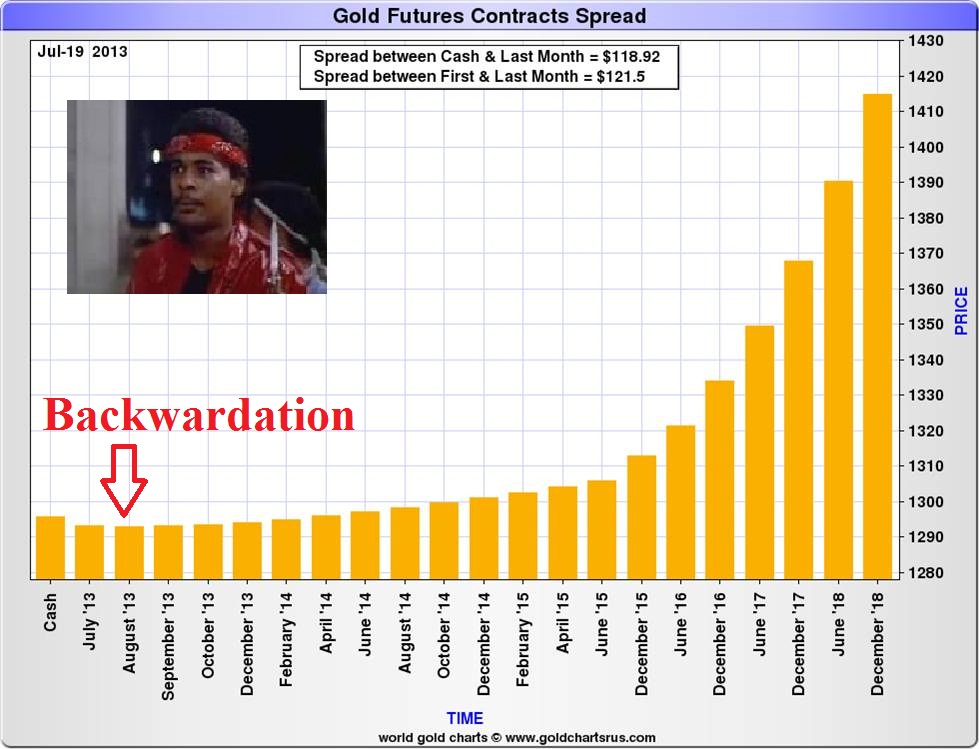

Backwardation of any sort should not normally occur in the gold market because of the available large above-ground supplies. The fact that gold backwardation is in fact occuring is highly significant. The now twelve days of negative GOFO rates suggest extreme tightness in the physical market in London. I find it somewhat strange that you are trying to downplay this..

Why do you think that this state has not been in this situation since 2008? And only a few times in the past decade.

The gold chart shows a long term uptrend in gold.However, in the short term the prices are lower. This is true backwardation. It defies the trend, and therefore indicates fear of near term gold supply failure.Another backwardation indicator is that the gold lease rate is higher than the Libor rate.

any construction (literal or figurative) built solely to deceive others into thinking that some situation is better than it really is

One of the most influential propaganda films of all time

The Author of the report you linked to works for the Perth Mint and he suggests that this might be more of a leasing market problem than a physical supply and demand problem he says...

Hmm.... When he sees 400oz bars attracting a 'special premium' he will let us know?The two biggest gold consumers India & China are paying a $30+ premium an ounce over spot, a 600%+ increase over what they paid in previous years!?

Hmm... When he sees bullion banks desperately bidding on Perth Mint's refining output he'll let us know? http://www.gold.org/ (Q2 Market update)

Hmm.. When he sees restrictions on how much gold can be bough he will let us know? 'the Reserve Bank of India banned import of gold by domestic consumers through bank credit' ' Gold coin and bar sales stopped in India' 'Pakistan temporarily bans gold imports'

Well I think the author has failed to disclose something... That he is blind!

As for the graph you linked to, just read the comments from the people who responded...

POTEMKIN:

'Potemkin Village':

'battleship Potemkin':

http://en.wikipedia.org/wiki/Battleship_Potemkin

http://en.wikipedia.org/wiki/Potemkin_village

I'm glad you read it and you observed he works for Perth Mint. Seems so...

Why is he "blind"?

China has been "gold crazy" for a very long time...

They are also nuts about US bonds and US dollars overall. How crazy!

I think he is blind because he says in his most recent blog, (http://goldchat.blogspot.co.uk/) that when these three factors happen

1. High Premiums

2. Unprecedented demand for mint output

3. Gold buying/ownership restrictions

Then you'll know it is more likely real backwardation and not just a gold leasing problem.

These points -

1. India & China are paying a $30+ premium an ounce over spot, a 600%+ increase over what they paid in previous years!?

2. The Perth mint reported the highest demand levels in five years

3. The Reserve Bank of India banned import of gold by domestic consumers through bank credit. Pakistan temporarily bans gold imports'

Are my points, not his, to show that those three things he is waiting for to happen are already happening.

Yes I see your Avatar is Battleship Potemkin,

But because of some dubious posts you've made, like finding the only guy who is blind to the crazy physical demand at the moment and making posts like this in the China thread -

It makes me wonder if you chose that name because you are deliberately trying to troll/downplay/'potemkin village' the PM situation at the moment.

")

I think he is blind because he says in his most recent blog, (http://goldchat.blogspot.co.uk/) that when these three factors happen

1. High Premiums

2. Unprecedented demand for mint output

3. Gold buying/ownership restrictions

Then you'll know it is more likely real backwardation and not just a gold leasing problem.

These points -

1. India & China are paying a $30+ premium an ounce over spot, a 600%+ increase over what they paid in previous years!?

2. The Perth mint reported the highest demand levels in five years

3. The Reserve Bank of India banned import of gold by domestic consumers through bank credit. Pakistan temporarily bans gold imports'

Are my points, not his, to show that those three things he is waiting for to happen are already happening.

Yes I see your Avatar is Battleship Potemkin,

But because of some dubious posts you've made, like finding the only guy who is blind to the crazy physical demand at the moment and making posts like this in the China thread -

It makes me wonder if you chose that name because you are deliberately trying to troll/downplay/'potemkin village' the PM situation at the moment.

Hmm.... When he sees 400oz bars attracting a 'special premium' he will let us know?The two biggest gold consumers India & China are paying a $30+ premium an ounce over spot, a 600%+ increase over what they paid in previous years!?

Hmm... When he sees bullion banks desperately bidding on Perth Mint's refining output he'll let us know?

Hmm.. When he sees restrictions on how much gold can be bough he will let us know? 'the Reserve Bank of India banned import of gold by domestic consumers through bank credit' ' Gold coin and bar sales stopped in India' 'Pakistan temporarily bans gold imports'

You found this thread quite fast. How come?

Welcome to the forum Mr. Bronsucheki. I'm familiar with your posts over at Silver Stackers. Cheers.

A real gold bank run will manifest itself in the wholesale markets for 400oz bars. When I see them attracting a premium and/or being difficult to source, or bullion banks desperately bidding on the Perth Mint's refining output, then we "have the real deal" as Dan says. I will let you know. just watch Bullion Vault and Gold Money - which are backed by 400oz bars and which deal in that market every day - for reports of difficultlies in getting 400oz bars and restrictions on how much gold can be bought, and/or if they start to add on a "special" premium to their spot price.

When I see... bullion banks desperately bidding on the Perth Mint's refining output... I will let you know

while yesterday HSBC released eligible inventory, today Scotia was forced to hand over registered gold straight into JPM's eligible pile: this is perhaps the first time we have seen this happen laterally between two vaults, without an intermediate warrant detachment step. Furthermore, with HSBC moving 43.4K oz from Registered to Eligible, we would expect either another major Comex withdrawal in the next few days from HSBC, or this is merely HSBC making room for further gold "requests" by JPM.

Just watch Bullion Vault and Gold Money... for reports of difficultlies in getting 400oz bars and restrictions on how much gold can be bought,

...

Most physical gold sold in Asia carries premiums, especially in India, and bullion banks are moving to fill that void in order to capture those lucrative premiums.

They are doing so by procuring physical gold in the U.S., not only from the COMEX warehouses and ETF liquidations, but directly from refiners. The gold is then converted into forms which Asians are comfortable with -- mainly kilo bars, and then the gold is shipped to Asia.

Several weeks ago I exchanged emails with a rep for a major precious metals refiner about the huge ETF liquidations and speculated that the liquidated gold was in fact going to Asia. After all, the gold coming out of the ETFs and the COMEX warehouses has to go somewhere.

The rep said that my speculation fit well with what his refinery was seeing. He said, “I think you are absolutely right given the level of large institutional demand we see for our kilo bars and 400 ounce bars that are going to New York and London.” New York and London are the off-loading sites for gold being shipped to Asia.

In another email, he said, “The bullion banks were buying as much metal from our company as they could get their hands on, just to ship to Hong Kong and Singapore.” So this is just further evidence that ETF and COMEX gold is going to Asia.

...

I had the chance to reconnect with a source in the bullion management business, whose operations deal on a direct basis with the shipping desks at the GLD. While remaining unnamed at this time, it was a powerful conversation, and he was quite liberal in sharing thought.

Speaking to what his group is hearing from the main GLD custodian, he noted that, “GLD is collapsing in [terms of] the number of share issuance, and [is] being redeemed…we are hearing from my end…that the GLD main custodian has been collapsing it and redeeming it, and that gold is just being shipped via their shipping desk directly to Asia.”

He further added that, “It is quite clearly a major establishment using their shipping desk to ship gold bullion, and potentially having it re-smelted down in Singapore, Hong Kong, etc. It (the gold) is moving.”

...

But to be blunt (And as I think you know full well yourself), the idea that you'll see the overt stress indicators that you suggest coming from the bullion banks actions themselves is quite frankly absurd because the day they show provable supply side issues is the day they default.

Which is why I showed how each of the indicators are already clearly manifesting themselves in the gold market. (& though you repeatedly try to pretend that there is this massive separation between stresses in demand in the retail and wholesale market, they are in fact completely interlinked.)

1. In times of demand stress the bullion banks are the ones supplying many mints with additional refining input never mind bidding on the output?

2. I'd imagine the bullion banks have preferential contracts in place and ones that prohibit you, a Perth Mint employee from disclosing market sensitive information, so I take your 'I will let you know' with a pinch of salt.

3. If the bullion banks were having issues, instead of people like Perth Mint employees letting the public know about it, I'd expect them to go out and try to convince people of the opposite - 'Don't worry there are not wholesale supply issues' & shi*, look, here you are...

So rather if I was looking for supply problems in the 400oz wholesale market, I'd look for signs of additional central bank leasing, particularly the Bank of England who are a key source of supply in times of stress. & shi* look a story just in the last two weeks that the BOE may have leased up to 1300 tons in the 400oz wholesale market in the first half of the year

Or I'd look for signs that Bullion Banks are running short of supply and/or are being forced to help one another out. & shi* look at how much of JPM's inventory has been removed this year and also this story from just yesterday

But as these don't constitute hard evidence, & people like Potemkin would say 'Rumours, words, stories...' I chose to bring up provable supply side shortages &/or unprecedented demand in the gold market which is of course what creates the wholesale market problems you are witnessing above.

Really!? How many hours do you think it will take from the time they announce purchasing restrictions to Gold Money to the time they default? I think you know that this is the very last thing they will do, if they don't actually just default first.

If there are demand stresses for gold, I think it's (painfully) obvious that they would rather do their best to try cut demand from the biggest gold consumer, India. (EDIT: Which is obviously why I brought up the restrictions in India and outright temporary import ban in Pakistan as being very indicative of shortages in the wholesale market.) As this would ideally (For the bullion banks) have the effect of decreasing demand for their good delivery bars in that market and also freeing up mint output sourced from the mines & scrap, so that it could then be used to refine new 400oz delivery bars for the bullion banks as opposed to coins and smaller bars for retail.

Bronsucheki, are you able to confirm or deny this claim (at least as it pertains to the Perth Mint) from Bill Haynes?

Nope, got that wrong. US Mint, yes needs to get metal from the market but the two other big ones - Canadian Mint and Perth Mint - are refineries so they source their own metal and in fact have excess left over after coining needs. Perth Mint refines around 6 tonnes a week and we use 10%, maybe up to 20% if lucky, for coin production. The rest we turn mostly into kilo bars and then sell it to the highest bullion bank bidder - it is that premium on kilo bars that tells us how desperate they are, in addition to where it is going and what form, gives a lot of info.

during the 2008 financial crisis... the Perth Mint was shipping in 20 tonnes of silver each week from London for about 20 weeks on end.

In India there are import duties and other taxes that go into the premium.

So I'm surprised during the period of unprecedented demand this year that you didn't have to source any additional supply from the LBMA in London again?

You also say the majority of your non coin production is being made into Kilo bars for the highest bullion bank bidder. But I was under the impression that the bullion banks dealt in the larger 100 & 400oz bars & that the 1 kilo bars would be more for the retail investment market?

But the import taxes/duties in India are 8% that would be $104 an ounce, far higher than the $30 premium the media is using. Doesn't this mean that the $30 premium is the premium they're paying prior to import duties/taxes being applied?

Bloomberg News television today lets Mihir Dange, co-founder of commodity trading firm Grafite Capital, remark that his company bought physical gold eight weeks ago but still hasn't gotten delivery yet. Dange says "there's a huge run on physical now." ...

Those sort of inter-bank transfers are standard part of market clearing http://lpmcl.com/

this is perhaps the first time we have seen this happen laterally between two vaults, without an intermediate warrant detachment step.

The Color-Coded Comex Crunch: Behind The JPMorgan Golden "Musical Chairs" Scramble

the only net exit of gold from the Comex took place at JPM. Everything else was, well, a "musical chairs" scramble to actually obtain the gold.

Those sort of inter-bank transfers are standard part of market clearing http://lpmcl.com/

The Indian restrictions aren't doing anything to stop demand, it is just being smuggled. The Indian Govt actions are just about making their CAD figure look better to financial markets.

this is perhaps the first time we have seen this happen laterally between two vaults

Today I see another negligible 4k ounces went from Scotia to JPM and JPM converted a massive 70k ounces from there 360k registered total and moved it onto their 100k eligible total.

Personally I think at the very least a Bullion Bank run is in progress at JPM and I think even though the writing is on the wall, the others are just trying to help JPM make it to some pre-determined end date.

My question to you is, having seen how these unusual transfers have continued since my original post do you still think

My question to you is would you agree that the banning of buying gold on consignment did have the effect of considerably decreasing India's overall physical gold demand for 1-2 months (incl. smuggling)?

...

The transfer from registered to eligible is why one needs to add both stocks together and compare that to open interest, which is what I did in this post. The current coverage ratio for gold is 17.7% and silver 24.5%. Looks like plenty of metal for redemptions.

...

Yes, as India had a relatively open gold import system the sudden rule changes crimped legitimate imports but the smuggling network was not in place to take up the slack so that would have had the net impact of restricting demand. We have recently seen a pick up in demand from other countries which tells us smuggling has started back up.

I disagree with Eric Sprott that western central bankers "called up" India and asked/told them to do these import restrictions to help them out. I agree more with Jim Rogers on this "Indian politicians who suddenly blamed their problems on gold. The three largest imports to India are crude oil, gold and cooking oil. Since they can’t do anything about crude and vegetable oil, the politicians said India’s problems were because of gold, which, in my view, is totally outrageous. But like all politicians across the world, the Indians too needed a scapegoat."

The finance ministry lifted the import tax on gold to 10% from 8%. The tax on silver was also raised to 10%, from 6%. India is the world's biggest gold consumer and a leading market for silver.

I disagree with Eric Sprott that western central bankers "called up" India and asked/told them to do these import restrictions to help them out. I agree more with Jim Rogers on this "Indian politicians who suddenly blamed their problems on gold...

The Indian Govt actions are just about making their CAD figure look better to financial markets.

Shanghai Gold Exchange ?

Shanghai Gold Exchange ?Gold demand fell 12% to a 4-year low of 856.3 tons in Q2, according to the World Gold Council. According to the report, central bank gold acquisitions fell 57%to 71.1 tons in Q2 and gold ETFs post outflow of 402.2 tons in Q2. Paulson & Co. cut its stake in SPDR Gold Trust in Q2, whilst there were also reports that Soros dumped his SPDR stake.... China July refined copper output at 534,600 tons.