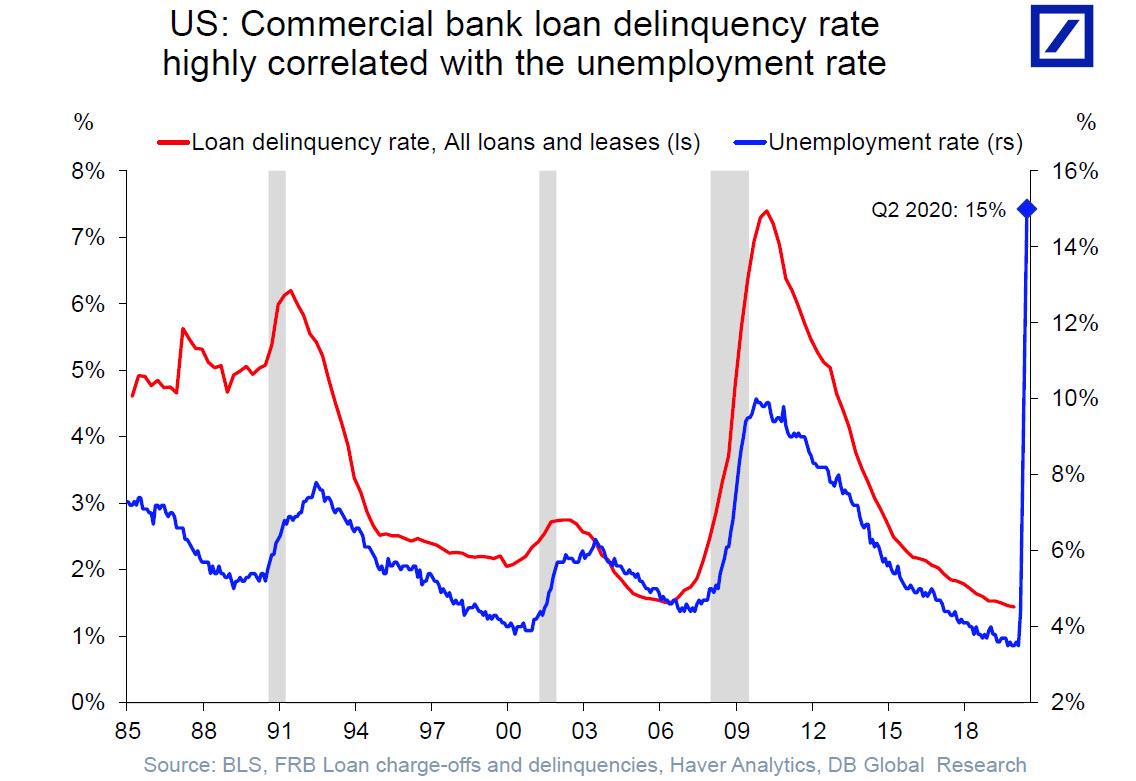

The U.S. Federal Reserve warned Friday that the financial sector faces “significant” vulnerabilities due to the coronavirus pandemic, as businesses and households grapple with fragile finances for the foreseeable future.

...

Friday’s report noted the financial stresses that could build if the crisis persists, and households and businesses continue to be deprived of wages and revenue.

In short, no one from hedge funds to major banks to households would be immune from the risk they might default on debt, be forced to sell off assets, end up in bankruptcy, or see the value of assets dwindle.

...

... Fed Governor Lael Brainard ... highlighted a key worry at the central bank: that what might start as a cash crunch could spiral into something worse. Among highly indebted businesses, she said, “we will be monitoring closely for solvency stresses...which could increase the longer the Covid pandemic persists.”

Few if any parts of the economy are safe. ....

“Financial sector vulnerabilities are likely to be significant, in the near term,” the Fed said. “The strains on household and business balance sheets from the economic and financial shocks since March will likely create fragilities that last for some time.”

https://www.reuters.com/article/us-...l-vulnerabilities-from-pandemic-idUSKBN22R34Y