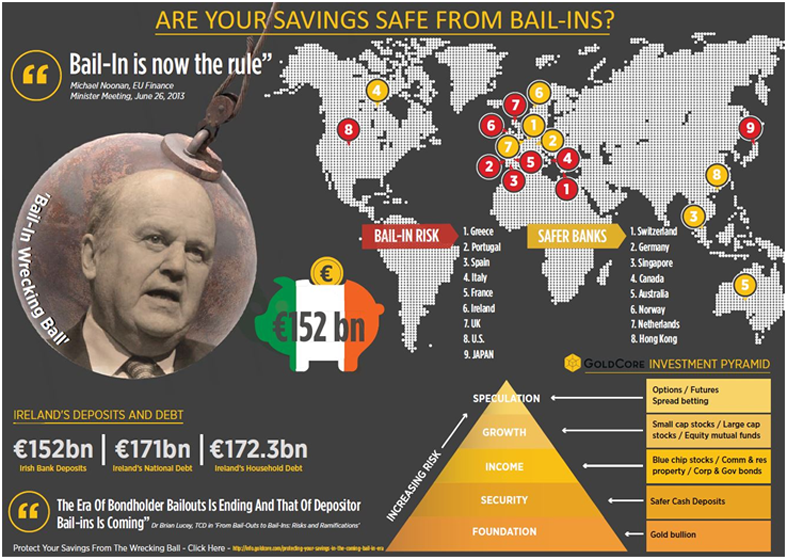

Following the news that TBTF Cypriot zombie banks will steal from depositors rather than go through normal bankruptcy, we heard that Canada was ready to abandon fiduciary responsibility too. Now there are reports that the USA and the UK have an agreement in place to do the same:

More: http://silverdoctors.com/fdic-bank-...limited-cyprus-style-bail-ins-for-tbtf-banks/

Wall Street bankers breath a sigh of relief as their multi-million dollar bonuses are now safe. Instead of losing their jobs when the bank is dissolved in bankruptcy, they are going to get fat on the backs of depositors.

Edit: I found the source document that SD is quoting:

http://www.bankofengland.co.uk/publications/Documents/news/2012/nr156.pdf

...

In the introduction, the resolution informs readers that the FDIC and the Bank of England have been working together to formulate the new bail-in model for future bank failures:The Federal Deposit Insurance Corporation (FDIC) and the Bank of England—together with the Board of Governors of the Federal Reserve System, the Federal Reserve Bank of New York, and the Financial Services Authority— have been working to develop resolution strategies for the failure of globally active, systemically important, financial institutions (SIFIs or G-SIFIs) with significant operations on both sides of the Atlantic.

The goal is to produce resolution strategies that could be implemented for the failure of one or more of the largest financial institutions with extensive activities in our respective jurisdictions. These resolution strategies should maintain systemically important operations and contain threats to financial stability. They should also assign losses to shareholders and unsecured creditors in the group, thereby avoiding the need for a bailout by taxpayers.

The joint US/UK resolution states that depositor haircuts are already legal in the UK thanks to the 2009 UK Banking Act:And that the legal authority has already been given in the US buried in Dodd-Frank:In the U.K., the strategy has been developed on the basis of the powers provided by the U.K. Banking Act 2009 and in anticipation of the further powers that will be provided by the European Union Recovery and Resolution Directive and the domestic reforms that implement the recommendations of the U.K. Independent Commission on Banking. Such a strategy would involve the bail-in (write-down or conversion) of creditors at the top of the group in order to restore the whole group to solvency....It should be stressed that the application of such a strategy can be achieved only within a legislative framework that provides authorities with key resolution powers. The FSB Key Attributes have established a crucial framework for the implementation of an effective set of resolution powers and practices into national regimes. In the U.S., these powers had already become available under the Dodd-Frank Act. In the U.K., the additional powers needed to enhance the existing resolution framework established under the Banking Act 2009(the Banking Act) are expected to be fully provided by the European Commission’s proposals for a European Union Recovery and Resolution Directive (RRD) and through the domestic reforms that implement the recommendations of the U.K. Independent Commission on Banking (ICB), enhancing the existing resolution framework established under the Banking Act.

The development of effective resolution strategies is being carried out in anticipation of such legislation. The unsecured debt holders can expect that their claims would be written down to reflect any losses that shareholders cannot cover, ...

More: http://silverdoctors.com/fdic-bank-...limited-cyprus-style-bail-ins-for-tbtf-banks/

Wall Street bankers breath a sigh of relief as their multi-million dollar bonuses are now safe. Instead of losing their jobs when the bank is dissolved in bankruptcy, they are going to get fat on the backs of depositors.

Edit: I found the source document that SD is quoting:

Resolving Globally Active, Systemically Important, Financial Institutions

A joint paper by the Federal Deposit Insurance Corporation and the Bank of England

10 December 2012

...

http://www.bankofengland.co.uk/publications/Documents/news/2012/nr156.pdf

")