...

Penny Crosman writes, "One is a heavy reliance on AML software to monitor transactions overseen by decision-makers who don't know individual customers. Another is outdated rules used to determine which transactions are suspicious. A third is a set of incentives that push banks to rush and not take the time to understand individual cases."

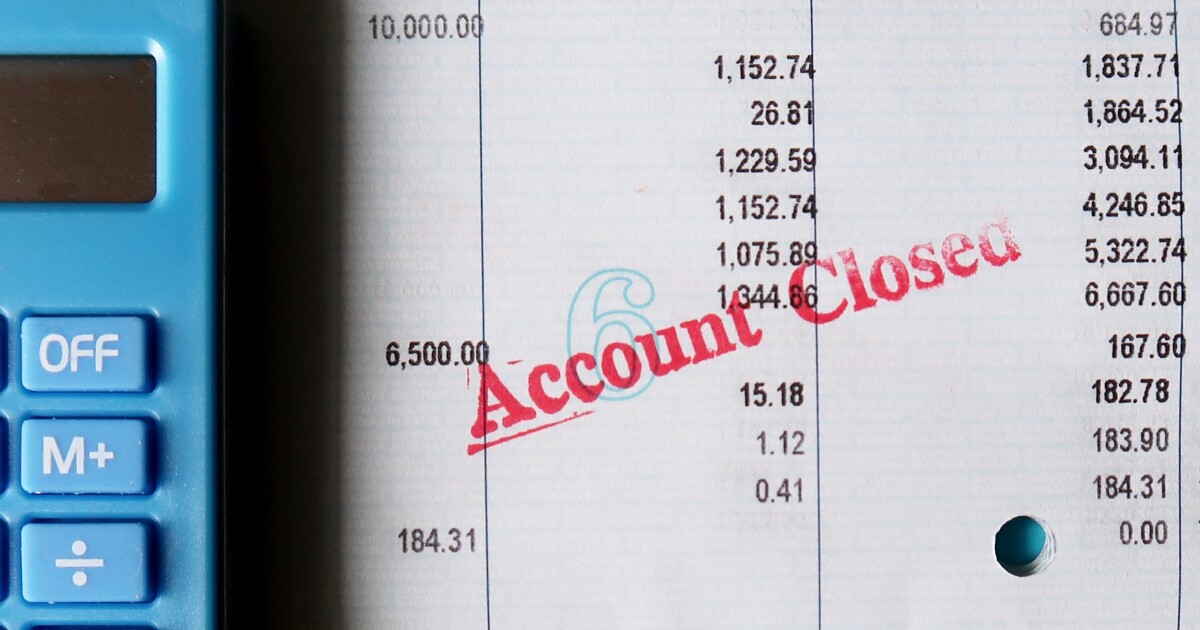

It's true that algorithms alert financial institutions to transactions that appear suspicious. Thomson Reuters found the number of suspicious activity reports (SARs) filed by banks surged by 50% in just two years. Rather than investigate the flags, however, there's a growing tendency to close accounts and shut customers out.

...

... In a risk/reward trade-off, we're led to believe it's too expensive to include customer input and losing a "minuscule" number of customers is preferable to the inevitable "regulatory headaches."

...

The human impacts of SAR processes gone wrong were captured by the New York Times in a recent examination of over 500 cases of customers being dropped by their banks. Small businesses can't make payroll, credit scores take a hit, people can't pay their bills on time — it's all very messy.

...

The rise in account closures reveals banks must rethink their processes

Banks cannot shrug off the impact of sudden account closures as inevitable collateral damage involved in fighting money laundering.

www.americanbanker.com

www.americanbanker.com

So anti-money laundering (AML ) software flags accounts that deal with cash. Banks then close the accounts for these customers (including perfectly legal coin shops) rather than spend any thought or effort to discern whether the AML software is flagging legitimate concerns.

Whoever controls that AML software holds the reigns to a stealth Operation Choke Point on all cash heavy businesses. The drumbeats for the cashless society beat on. Is America listening?