How's the JPMC - Treasury matchup looking?

My money's on Treasury.

My money's on Treasury.

Welcome to the PMBug forums - a community supported watering hole for folks interested in gold, silver, precious metals, sound money, investing, market and economic news, central bank monetary policies, politics and more.

Register a free account to join the discussions. When you register an account and log in, you may enjoy additional benefits including access to market data/charts and additional members only rooms (including one for trade/barter with the community).

... Where is the money going?

The answer starts with money-market funds, low-risk investment vehicles that buy short-term government and corporate debt. These saw inflows of $121bn last week as svb failed. However money does not actually enter such vehicles, for they are unable to take deposits. Instead, cash that leaves a bank for a money-market fund is credited to the fund’s bank account, from which it is used to purchase the commercial paper or short-term debt in which the fund invests. When the fund uses money in this way, it flows to the bank account of whichever institution sells the asset. Inflows to money-market funds should thus shuffle deposits around the banking system, rather than force them out of it.

And that is what used to happen. Yet there is one obscure way in which money-market funds may suck deposits from the banking system: the Federal Reserve’s reverse-repo facility, which was introduced in 2013. The scheme was a seemingly innocuous change to the financial system’s plumbing that may, a decade later, be having a profoundly destabilising impact on banks.

In a usual repo transaction a bank borrows from competitors or the central bank and deposits collateral in exchange. A reverse repo does the opposite. A shadow bank, such as a money-market fund, instructs its custodian bank to deposit reserves at the Fed in return for securities. The scheme was meant to aid the Fed’s exit from ultra-low rates by putting a floor on the cost of borrowing in the interbank market. After all, why would a bank or shadow bank ever lend to its peers at a lower rate than is available from the Fed?

...

The Federal Reserve will be forced to make an "emergency rate cut" by June, according to Edward Dowd, former BlackRock portfolio manager and Founding Partner of Phinance Technologies. He predicted that a "controlled implosion" of the banking sector would follow over the next 24 months, leaving the United States with only six major banks.

...

"They [the authorities] are going to continue to play what I call "whack-a-mole," he said. "They plug their finger in the dike, everybody breathes a sigh of relief, and then there's another problem… I'm hoping that's the case because to be honest, I don't want to see a fast panic. That's not good for any of us."

The result of this, forecast Dowd, is that only six banks would be left standing, making it easier for the government to introduce Central Bank Digital Currencies (CBDCs), programmable tokens issued and controlled by central banks, and which operate as fiat currency. He claimed this would all occur by 2025 at the latest.

He also predicted that, based on the year-over-year growth rate of the M2 money supply, a "hard recession" will soon manifest, prompted by "continued economic deterioration," "more bank failures," and a possible global "sovereign debt crisis."

To find out why Dowd thinks the upcoming recession he forecasts may be comparable to the Great Depression, watch the video above.

Central Bank Digital Currencies

"If you wanted to introduce central bank digital currency, wouldn't it be better to have only six banks in the U.S., all systemically important, basically run by the government?" Dowd suggested.

...

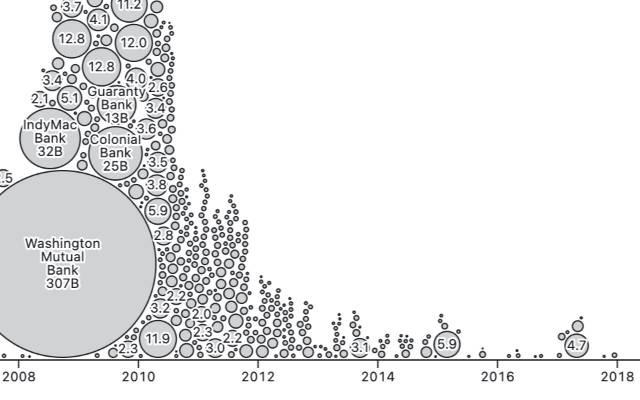

Banking-sector jitters are on the minds of depositors, investors and policy makers, but how do the current problems compare with bank troubles through history? Over the past eight centuries, researchers say, there are few direct parallels for the particular twists and turns of recent weeks.

But when past bank troubles were most similar to current events, the financial pain ended up being widespread most of the time, according to researchers at the Yale School of Management and Boston College’s Carroll School of Management.

Taking the very, very long view, Andrew Metrick at Yale and Paul Schmelzing at Boston College have spent several years compiling the ways governments and markets have responded when banks looked shaky and anxiety ran high during the past eight centuries.

Out of 880 crises affecting 138 countries, they found 57 events echoing the current moment, where account guarantees and emergency lending were the tools regulators and banks used to calm nerves.

That’s 6.5% of the sample size, they noted in a Monday study released by the National Bureau of Economic Research. It’s a “relatively rare occurrence to see such a particular policy mix deployed,” the study said.

Just over half of all the 880 crises turned out to be systemic and far-reaching, they noted. But of the 57 similar historical episodes — which include America’s financial turmoil in 2008-2009 — nearly 80% turned out to be widespread and systemic, they noted.

...

As the old saying goes, you can hope in one hand and umm, do something else in the other?I hope he is wrong.

When push finally meets shove, it'll suck to be them.The FDIC has confirmed that none of the $622.607 billion in deposits in foreign offices/branches of Citibank are FDIC insured.

Moody's Investor Service has downgraded the U.S. banking sector by one notch as the sector faces higher interest rates, funding risks and less credit strength, on the heels of earnings updates from financial firms in recent days.

Citing deterioration of the operating environment and pressure on profit margins, Moody's late Friday cut its macro profile of the U.S. banking system to "Strong+" from "Very Strong-".

"There are negative credit implications for the U.S. banking sector that extend beyond immediate funding challenges to downward pressure on banks' earnings, combined in some cases with weaker capitalization and risks related to commercial real estate (CRE)," Moody's said.

Moody's downgraded 11 banks including Comerica Inc. (CMA), U.S. Bancorp (USB), First Republic Bank (FRC), Western Alliance Bancorp/ (WAL), and Zions Bancorp. (ZION).

...

mishtalk.com

mishtalk.com

I know several people with more than 250k in their accounts that have moved the majority to money market accounts for safety and yield.Jim Bianco says we're seeing a "bank walk" in all banks (actually worse in larger banks than smaller ones) as people withdraw accounts to chase yield in money market funds:

A Tidal Wave of Money Leaving Banks Will Kill Bank Profits and Lending

Jim Bianco has a 21-Tweet Thread on what’s going on with bank deposits. I chimed in on a couple of the Tweets. Here are some of the most important ideas.The “bank walk” becomes a …

www.reuters.com

www.reuters.com

...

The solution that emerged early Monday morning deals with the immediate threat of a disorderly failure of First Republic and, therefore, does not fuel the already uncomfortable risk of possible additional disruptions to other regional and community banks.

Yet the potential collateral damage and the unintended consequences are far from immaterial.

Four stand out in particular.

...

- First, the US now has a more concentrated banking system, with what was once viewed not so long ago as “too big to fail”/”too big to manage” banks becoming larger.

- Second, there is even greater doubt about the nature of the de facto deposit insurance system in place.

- Third, the compositional risk within the banking system of less credit extending into the economy will continue, potentially aggravating the headwinds to high and inclusive growth.

- Finally, the total cost of First Republic’s resolution remains to be assessed, including how the burden be shared among the public and private sectors and, with that, the extent of the “bailout” for the 11 banks that had large deposits with First Republic.

www.zerohedge.com

www.zerohedge.com

As announced on March 15, 2020, the Board reduced reserve requirement ratios to zero percent effective March 26, 2020. This action eliminated reserve requirements for all depository institutions.

...

Dats whys da' in charge! Da smart!Smart.

Understatement of the year!Yeah, this banking crisis is not over yet.

PacWest and Western Alliance each saw their shares drop more than 25% early Tuesday, a sign that fears about the health of regional banks are still running high after First Republic was seized and sold to JPMorgan.

PacWest and Western Alliance—which were temporarily halted for volatility as they plunged— have been among the hardest-hit banks in the turmoil. Both banks reported double-digit quarterly declines in deposits at the end of March, but said flows have since stabilized.

...

Western Alliance Bancorp. led a rebound in regional bank stocks Wednesday, after an analyst said the recent selloff on the heels of the distressed sale of First Republic Bank to JPMorgan Chase & Co was “irrational” given hard numbers from the bank on its relative stability.

...

www.zerohedge.com

Oops..

ZeroHedge

ZeroHedge - On a long enough timeline, the survival rate for everyone drops to zero

www.zerohedge.com

Hedge fund manager and macro economic expert Hugh Hendry just issued a major warning on the US banking system and the American economy as a whole.

In a new interview on Bloomberg Markets, Hendry says mass panic and capital flight away from the US banking sector is entirely justified.

Hendry says a further decline in the M2 money supply, which in part tracks money in liquid checking accounts, could convince the US government to step in and prevent citizens from taking their capital out of the banking system.

“Sometimes it’s kind of relevant to panic. I would recommend you panic… You’ve seen the biggest waterfall decline in M2 right now. M2 is deposits, not loans. That’s the deposits fleeing the system and going into money market funds.

That could reach a crescendo where the Treasury and the Fed may have to come in and actually restrict your right as a US citizen to pull money out of the US banking sector.”

dailyhodl.com

dailyhodl.com

It's happened before.It's hard to imagine it happening, but that doesn't mean it can't.